Lower turnover, predictable monthly revenue, B2B demand from insurance and corporate companies, and a flat 8% booking fee instead of an annual subscription. The economics shifted in 2025.

For most of the last decade, the conventional wisdom was simple: short-term rentals (STR) are where the margin is. Higher nightly rates compounded across more turnovers beat anything you could get with a traditional 12-month lease. The "STR arbitrage" model was its own genre.

That math is changing. Three things shifted between 2023 and 2026 that make midterm — 30+ day furnished stays — look meaningfully better for many Hosts:

This post is the breakdown. We'll keep it Host-centric.

One honest caveat up front: if you're a top-decile STR operator in a market that hasn't regulated — high nightly rates, near-full occupancy, a turnover machine that runs itself — STR-only may still win for you. For everyone else, the case for committing to midterm is getting harder to argue against, and the reason is supply. Furnished 30+ day inventory is far thinner than nightly inventory, so rates hold up better than people expect and the demand is easier to win than the nightly scramble.

A nightly listing booking 60% of the year sounds great until you count the operational cost of every check-in: cleaning, restocking, key handoff or smart-lock troubleshooting, occasional damage. A 30+ day stay does that whole cycle once. A nightly stay can do it 30 times in the same month.

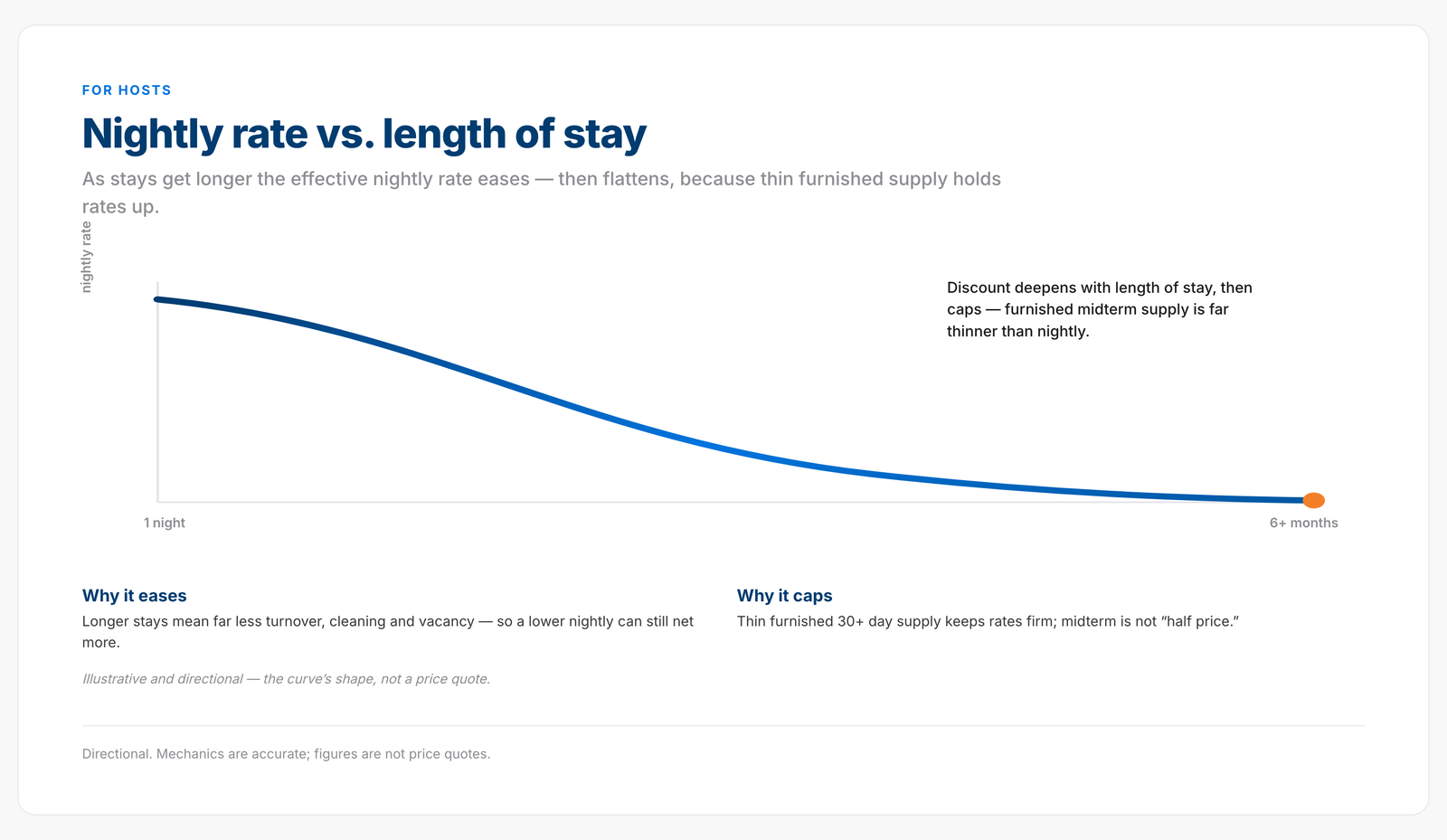

Start with the rate, because the "STR pays double" instinct is mostly wrong. Midterm isn't half-price. The discount to a comparable nightly rate is shallow for a one-month stay and only deepens with length of stay — and it's capped, because thin furnished supply holds rates up. As a real-world anchor: in Austin, independent market data (AirDNA/AirROI, trailing 12 months to May 2026) put short-term ADR around $266–$288 versus a median furnished nightly near $187 — and that ~30–35% gap is the deep end (long stays; median-vs-mean overstates it), not the typical case. A one-month booking sits far closer to nightly pricing than that.

Now layer in turnover. A 30+ day stay runs the full check-in cycle once; a nightly calendar runs it again and again the same month. Even where the nightly rate is higher, the net gap narrows once cleaning spend and your team's time are in the math. Midterm isn't always the higher gross — it's frequently the higher net.

Cities that allowed near-unlimited STR in 2018 are mostly enforcing 30-day-minimums, primary-residence rules, or hard caps in 2026. Even in friendlier markets, regulatory uncertainty is now a permanent overhead — Hosts who built around STR carry exposure to ordinance changes that don't apply to midterm.

A unit listed for 30+ day stays is, by definition, on the right side of every "minimum stay" ordinance in the country. That's not nothing.

Three demand channels now drive midterm:

All three have grown materially through 2024–2026 — driven by hybrid work, post-pandemic relocation patterns, the climate-driven uptick in insurance claims, and the structural shortage of affordable housing in target markets.

Listing platforms broadly fall into a few fee models: an annual subscription where the platform doesn't run the transaction (you collect payment yourself, off-platform); a per-booking commission that scales with revenue and includes the transaction; or Radius's model — a flat 8% booking fee, paid by the Host, with the booking running 100% on-platform (search, rates, payment, confirmation), no annual fee, charged only when a stay actually books.

Exact head-to-head fee figures shift by plan, listing type, and who's collecting payment, so we won't pin a number on another platform here. The structural difference is the point: a flat per-booking fee with the money movement handled for you, versus a subscription where the payment rail is your problem, or a percentage that climbs with the rate.

If you're a Host considering the midterm shift, the practical changes:

This isn't all-or-nothing. Where you land on midterm is a spectrum, and most Hosts move along it over time:

The further toward full commitment you go, the more of the thin-supply advantage you capture — because the company-paid channels filter hard for Hosts who can actually hold the dates. For most properties the revenue-maximizing point is somewhere in the middle, not the extreme; the spectrum is a map, not a sales funnel. You can connect an existing Airbnb listing so the same details and calendar run on both platforms with no re-entry; details are in the Radius help center at help.bookradius.com.

The shift toward midterm isn't speculative. It's already happening to most Hosts who took on STR over the last decade. The question is whether you take advantage of the demand or stay locked into a model the regulators are slowly walling off.

Book a 30+ day furnished stay, or list a property and reach insurance, corporate, and healthcare demand on one platform.

The Only Real-Time Marketplace Exclusively for 30+ Day Stays

© 2026 Radius. All rights reserved.

The only real-time marketplace exclusively for 30+ day stays.